Table of Content

Long-term care insurance makes in-home care the ideal choice when a policyholder wants to maintain independence in a familiar environment while comprehensively covering the costs of personal assistance. Navigating the benefits of these policies can unlock flexible care solutions tailored to your specific daily routines. Understanding your coverage details ensures you maximize the financial resources available for staying comfortable at home.

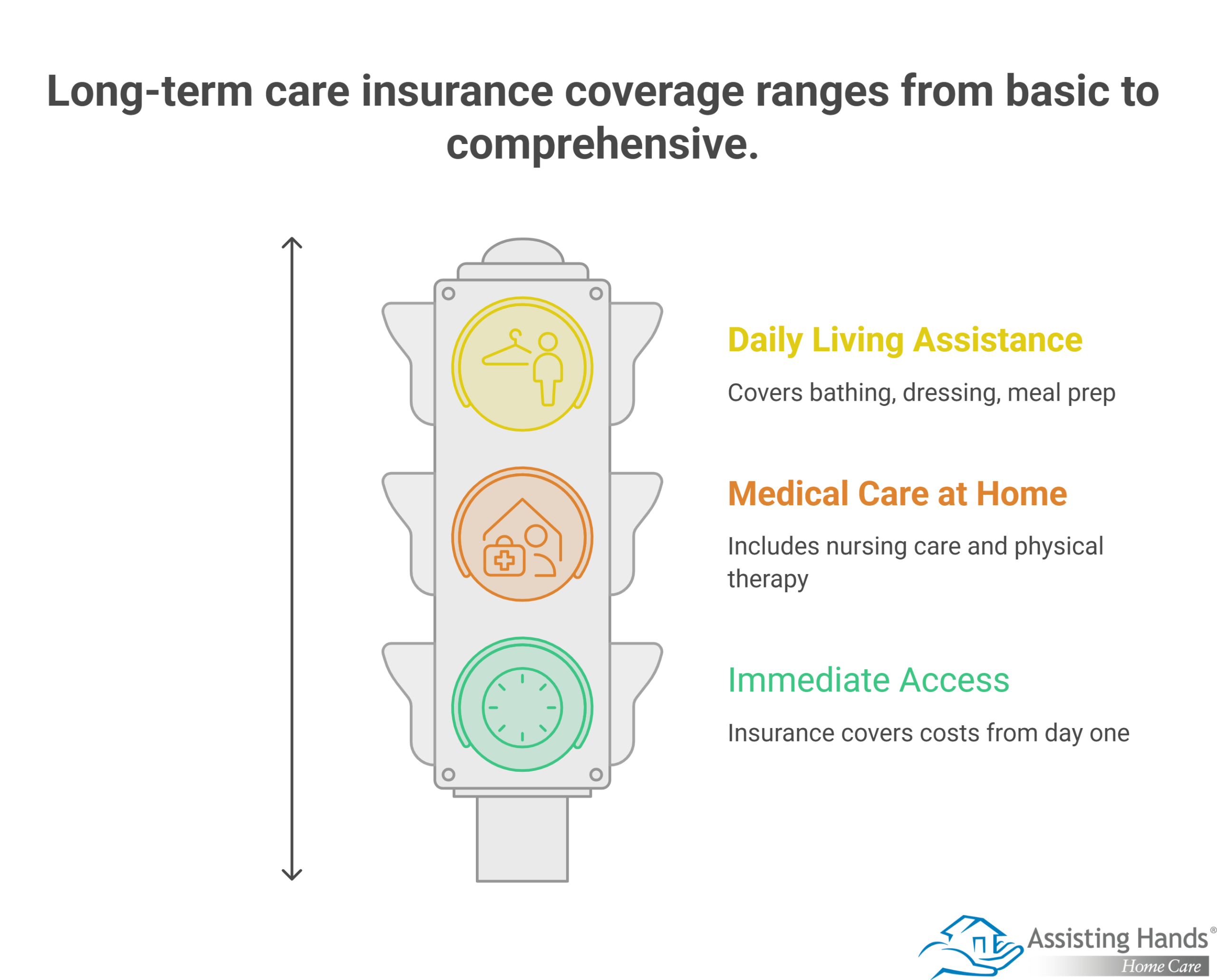

What Types of In-Home Services Does Long-Term Care Insurance Cover?

Most policies cover a variety of personal care and daily living assistance tasks. This typically includes help with bathing, dressing, meal preparation, and light housekeeping. Some specialized plans also pay for skilled nursing care or physical therapy delivered right to your door, ensuring your medical and personal needs are met simultaneously.

How Do Elimination Periods Affect Your In-Home Care Strategy?

An elimination period functions like a deductible based on time, requiring you to pay out of pocket for a set number of days before the insurance company begins reimbursing you. Choosing in-home care during this window is often significantly more affordable than entering a nursing facility.

- Shorter elimination periods mean faster access to your insurance funds.

- Home care allows for part-time or flexible scheduling to stretch your budget during the waiting period.

- Some policies have a zero-day elimination period specifically for home care services.

Many seniors prefer aging in place over moving to assisted living facilities. If you or a senior loved one needs assistance to remain safe and comfortable while living at home, reach out to Assisting Hands, a leading Home Care Fort Lauderdale agency. Our dedicated in-home caregivers can assist with meal prep, bathing and grooming, exercise, medication reminders, and many other important tasks.

Why Does Staying at Home Maximize Your Total Benefit Pool?

Many long-term care policies have a maximum lifetime benefit limit capped at a specific dollar amount. Because hourly home care generally costs less than full-time residential facilities, your designated funds will stretch over a much longer timeline. This approach preserves your financial safety net for future healthcare requirements.

What Are the Triggers Required to Activate Your Home Care Benefits?

Insurance providers typically require proof that you cannot perform a certain number of activities of daily living (ADLs) without physical assistance or supervision. Common ADLs include eating, transferring (moving from a bed to a chair), bathing, and toileting. A licensed healthcare practitioner must certify your condition and develop a formal plan of care before the insurance company approves your payouts.

Some seniors only require help with a few daily tasks so they can maintain their independence. However, those living with serious illnesses may need more extensive assistance. Luckily, you can rely on the exceptional professional Fort Lauderdale 24-hour home care provided by Assisting Hands Home Care. Home can be a safer and more comfortable place to live with the help of an expertly trained and dedicated around-the-clock caregiver.

Fort Lauderdale overnight care and respite care are a great help to many seniors and their families. Caring for a senior loved one can be overwhelming at times, which puts family caregivers at risk for burnout. However, an in-home caregiver can take over care for you or a senior loved one, allowing family members the time they need to focus on their own health, maintain full-time jobs, or care for other members of their families. To create a customized home care plan for yourself or a loved one, call Assisting Hands Home Care today.

Frequently Asked Questions

Does Medicare cover the same in-home services as long-term care insurance?

+

Medicare generally only covers short-term, medically necessary skilled nursing care or therapy. It doesn’t cover the ongoing personal assistance and custodial care provided by long-term care insurance.

Can I hire a family member to provide my in-home care?

+

Some long-term care policies include specific provisions that allow you to pay family members for caregiving. You must verify your contract details, as many standard policies require you to use licensed home care agencies.

Will my premiums increase if I start using my in-home care benefits?

+

Most modern long-term care insurance policies feature a waiver of premium clause. This feature actually stops your required premium payments entirely once you begin receiving covered benefits.

What happens if my home care needs exceed the daily benefit limit?

+

You’ll be responsible for paying the difference out of pocket if your daily home care costs surpass the specific daily maximum outlined in your policy.